When it comes to saving money, most of the citizens from sub continental countries are good at it. It comes naturally to most citizens in India to save money as well. ‘Save for the rainy days’ was one of the common teachings we received. As India progresses and our society moves towards being more modern, we need to re think of tips and tricks to save money in India.

Saving money need not come with a negative attitude or worse with a stingy attitude. If you are smart about money management and plan things out well to follow the tips and tricks, you can enjoy life and yet save money. Saving money is something smart and intelligent move to do. Yet you must make sure, you do enjoy your share of good life.

Let’s begin with why do we need to save money. For those who want to jump directly to the tips, please click the links below to scroll to the appropriate section. Otherwise, you can continue enjoying the read – beginning with the basics of saving money.

Table of contents:

- Benefits of saving money.

- How do I begin saving money in India for beginners.

- Other money saving ideas and tips in India

- How to start saving money when you are on a tight budget

- Power of compounding- Save your money the best way

Benefits of saving money.

1. You have financial independence and freedom

If you begin saving money, you build a buffer of wealth that you can fall back on some day. As you accumulate more, you are some what independent financially and have some freedom.

You stop worrying about day to day tasks related to money and it falls to the back of your mind. You rest peacefully, knowing that, say something like you loose your source of income or job (touch wood), you will be not be in a disaster the very next moment.

2. You are taking care of unforeseen financial circumstances:

Most things in this world do not come to us with a warning. Sometimes, even with very sound planning, some unforeseen incidents might pop over. You may need some emergency financing during such instances. If you have built your savings gradually, this can be taken care of.

3. You’ll be more comfortable during retirement.

Agreed, we don’t know how many years we will live. But the matter of fact is that the world population isn’t decreasing. The average human age has increased over the last decade. So there lies a fat chance that you’ll survive for a long run and will need finance to live a comfortable life.

Most of us, will not be as productive and physically strong at our old age. If you have some financial backing, you can live a better and comfortable life. It’s a good move to save for your old age.

For those, who say they don’t want to live for long- well, we would debate to at least get started with your old age savings. In worst cases, you could donate the savings to some needy child when you depart and work towards a good deed : )

4. Money saved is money earned

This is an old saying from Benjamin Franklin- ” A penny saved is penny earned”. This school of thought is more important in our modern day India. Most of us Indians are falling for modern day consumerism and material possessions.

Agreed- we do need modern tool to get your jobs done. However my friends, there also lies a small line between purchasing what you need v/s purchasing all that you can.

Now, say if you walk into a convenience store on a summer afternoon with a friend to lunch your thirst. You were desiring to purchase some water. The purpose of you walking in was to quench your thirst. If you have option of clean water sold for 50 rupees v/s a sparkling water bottle for 150 rupees. By purchasing what you need and not falling for the gimmicks, you have made 100 rupees in your wallet 🙂

When you purchase a new mobile phone or any gadget for that matter, the moment you have swiped your card and walked out of the store, the value of your purchased device has depreciated. In very less cases, could you get the amount you paid for it back by selling the device.

However if you never needed that device, you could have saved your money my friends. Before you purchase anything – do think if you really need it or can do away with something less cheap.

The below ones are for our young Indians.

5. Save for your future education

Education expenses has risen in India. Tertiary education cost has been on a very upward trend and many of our students in India have to depend on student loans.

However as a student; if you start planning for your own education , you probably will save enough and not require a student loan.

The pressure of to be paid student loan is too much for some of us. When we are done, we have to focus on getting a job sooner to pay back the loans. Also not to say, our other financial planning gets impacted with this loan. If you plan and save for your education, this will help you be financially independent sooner.

6. Save for your future home

It is dream for most of us to have our own home. The prices of home have risen in various cities in India as well.

Starting saving at a very young age would give you enough room to purchase your first home earlier in life. Do make sure you save in the best accounts that help you fight inflation.

Saving money starts today. Remember, even if you start saving a rupee- you have begun. It does not take a lot of stash to get started on savings. Make sure you read ahead to know how to best save the money so that it reaps benefits even when it is under savings mode.

How do I begin saving money in India for beginners.

As we said earlier, you can start today by just allocating some part of your income to savings. If you are a student and don’t have any income yet- you begin allocating your pocket money or any other sources of money like gifts you get.

1. 50/30/20 Budgeting

It all begins with proper budgeting. Budgeting is planning. When you have a plan, you know what the next steps you are supposed to take.

When you don’t have a plan in place, most of us usually go with the flow and that is where our money goes with the flow as well. Unintentional money flow- need not say ! For beginners, we would propose the 50 30 20 budgeting rule.

The 50 30 20 rule, suggests that you allocate 50 percent of your income to necessities, 30 percent towards your wants and 20 percents to your savings.

As you accumulate these savings, put them in high returns savings account or fixed deposits.

We have built a simple calculator here, which allows you to enter your monthly income and easily calculate your allocation to savings. Check out our 50/30/30 Budget calculator here.

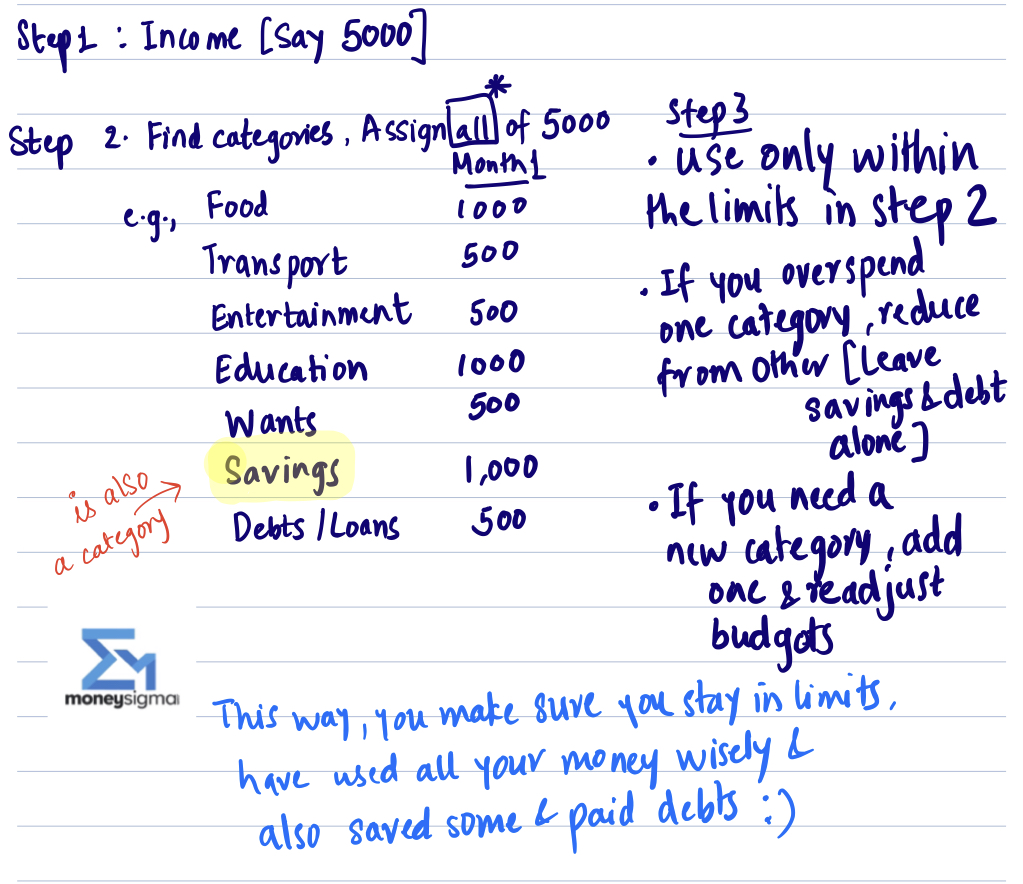

2. Give every rupee a job rule.

This style of budgeting is for those, who tend to spend a lot as soon as we see some spare money in our hands. Or those of us, who just don’t give it a second thought- when we see something we desire and is on a marketing sugar coated sale.

Giving every rupee a job, works on the idea of allocating all of your income and assigning spend categories to it. That means you use 100% of your income and allocate it giving everything a job. Say for example, you plan to use x amount of money on food, y amount on travel and z amount of savings etc. where x+y+z is all of your income. Not a single rupee is spared. Savings is also one of the category you assign to your income.

Since you have allocated 100% of your income, you will not have a chance of spending on anything random.

The below chart explains the rule with an example.

The rule of giving every rupee a job, is popular with the YNAB budgeting software. It is not necessary to use this software. A simple excel sheet will do the job and also help you save money.

3. Get your first bank account if you don’t have one yet

There are quite a number of us Indians, who don’t have a single bank account. Getting a bank account opens you to lots of financial savings possibiltles.

Having a bank account keeps your organised on your money management. If you are a student or an adult who never had a bank account, get one today my friend ; )

4. Saving money by using a second bank account

This trick or suggestion comes from a personal experience of mine. I have noticed that I started saving by automating this rule and had no excuses to not do so.

Most of us beginners will start with one bank account. This bank account is linked to our debit cards and is used for every payment we make. The problem with just one bank account is the liberty it gives you to spend funds as and when you wish.

With your savings in the same account, you do not have a clear idea of your limits on spending.

Say for e.g., you have 50,000 rupees in your bank account. Out of this 50K, 35,000 is savings. So in reality you can only spend 15,000. However when you swipe your cards or check your account balance, you see 50,000 and that gives you a false impression of money you can spend.

If you have a different account, solely meant for savings, the 35,000 would be out there. It would be out of your sight and not linked to your daily card and account. Thus next time you check your normal account, you do know, your spending limit is only 15,000.

The success to this strategy lies in automating the savings to your dedicated savings account. This way you don’t even make another excuse of not transferring the savings to that account.

Of course- in India, we have the minimum balance that needs to be maintained in bank accounts. You will need the total amount of money to easily open and maintain two bank accounts . Do this- if you can afford it. We don’t want to loose some of our income on fines for not maintaining the AQB or average quarterly balance.

But if you do have that much amount of savings, do try this tip and let us know, if it helped you too. Sometime’s small tricks moves mountains.

Other money saving ideas and tips in India

These are small tips and tricks to use in your daily lives, that will help you save money.

Tips for saving during Shopping

1. Budget your shopping spend

Follow the budgeting methods and allocate some pre defined amount to shopping. If you do not allocate a budget or a limit, chances are you’ll end up spending more than needed.

Most marketing messages and ads trick our brains to fall for gimmicks. However, when you have a pre defined limit, it puts an extra check on you.

2. Shop only with a pre written list

When you do visit a physical store to shop, making a list of stuffs to buy before you enter makes you stick with your purchases. I bet most of the big stores in India, try to arrange their goods in a way that you’ll fall to purchase them even if you don’t need it.

You go ahead to buy biscuits, but end up buying some sweet drinks as well- all because it was placed besides the biscuits. When you had a list in your hand and a budget to it- this might make sure you’ll stick to it. Most of our phones today have todo list apps. Do make sure you download some and make use of it. You need not purchase a fancy app for this my friends. Remember the intention of getting things matter.

3. Online Shopping only during limited allocated time and Disable notifications

Online shopping has boomed in India. And with those discount emails and notifications pouring in- we are getting addicted to online shopping. One trick is to disable all the notifications.

Do try it and see , how much calmness it brings to your life.

Well the point here is, limiting your time for online shopping will stop you from falling prey to mindless shopping. If you are addict on online shopping and do not know where to begin- start with moving these apps away from your home screen, disabling the notifications and only shop for an hour or two on a pre defined day of the week.

4. Use apps like Paytm etc to collect cash backs.

The boom of payment apps like Paytm in India, has led to various cash back use cases. Make use of those to save money.

However- the following part is very important- Please do make sure, you don’t fall into a shopping spree due to cash backs. Collecting cash backs, leads you to purchase more.

5. Use credit cards- don’t fall prey to their marketing.

Using credit cards with no annual fees and spreading out your expenses will also help you save money. However, purchase only what you can afford. Do not purchase anything on credit that you can’t afford to purchase.

Credit card marketing also comes with various strategies to get you to spend more. Make sure , you do not fall for these and purchase only what you need.

6. Time your major purchases

You will for sure have lots of discounts and promotions going around on flipkart.com and amazon.in, during Diwali, Christmas, Eid, Independence Day sales etc.

Various other stores also have their own promotions during festive seasons and throw in discounts then.

If you can time your purchases during these seasons, you can enjoy these discounts and save money.

7. Calculate your purchase based on hourly income

Whenever you are wanting to purchase big items you know you probably don’t need, try the hourly income strategy to decide.

Divide the cost of the purchase by your hourly income. This will give you the number of hours you have to work to purchase that device.

Often times, knowing the number of hours you have to work to get it, makes it worth less in our eyes. This might help you decide on your wants and needs in a better way.

How to save on Telecommunications

1. Switch to prepaid than postpaid

The cost of owning a pre paid phone card is way cheaper than post paid cards in India. Prepaid telephone cards are more accessible and affordable in India than most countries.

Post paid cards gives you unlimited usage, and that’s something which doesn’t go well with the rule of budgeting. With various apps and better internet connectivity in India, topping up your prepaid cards is more easy and accessible now a days.

2. Do you really need two phone numbers

Well, this is something that depends from person to person. Some of us do genuinely might need two phone numbers, but if you don’t and there is no need to have two, switch to single phone number. Do let us know, what’s your take on this .

3. Merge internet, phone or tv providers if it helps save money.

Telecom providers might bundle in various services at a cheaper cost if you bundle in internet, phone and tv service with the same company. Check if there are any such promotions and take advantage if so.

Tips for saving on clothing

1. Buy few but quality clothes

With the fashion shopping spree, most of us end up buying clothes that you might use only once or twice. That is not good on your wallet as well as on the environment.

Producing clothes, does impact the environment and it’s always best to do our part for Mother Earth. Buy quality clothes which you’ll use for good. Appreciate the quality and own them like some of our tech focused Indians own their gadgets 🙂

By buying quality (Not necessarily the most expensive at the store. Do learn to spot quality over price) clothes, you’ll spend less on the long term.

2. Staying clean is important. Please do wash your clothes- optimise it.

Staying clean is important my friends. Washing our clothes is important to keep it clean. Unclean clothes really makes one unpleasant. Optimise the washing process by pairing your clothes appropriately in your wash cycles.

Money Saving ideas on Household stuffs

1. Check on your electricity consumption and water usage

Having an eye on unmonitored electricity usage will also save you money on the long run. The weather in India varies. If you do have some air conditioning or heating at your home, monitor for leaks.

Fix leaks in your windows and doors to better insulate the area.

An easy trick is to light a candle and move it around the door and window frames in your home by closing them. If it flickers there is a flow of air coming in.

Leaking water costs you more than you think. Even though it might seem as a small leak, a leaking tap can cause thousands of litres of water to be wasted yearly.

Inspect water taps, toilet bowls, hidden corners under the kitchen etc and make sure there are no signs of leakage. Regular maintenance and cleaning will help you save money on the long run.

2. Install LEDS compared to normal lightings

Energy-efficient light bulbs might cost a bit more initially, but they have a much longer life than normal incandescent bulbs and use far less electricity.

LEDs are expensive, however they are getting cheaper day by day. LEDs can last for decades. Checking on lightings and your electricity usages will help you save money as well.

How to save on Transportation cost

1. Use public transport if its available and cheap.

Check on the costs of owning a vehicle, it’s insurance, fuel and maintenance to the number of public transport rides you can check if it makes more sense for your economics.

If opting for public transport helps you save money do so.

However, if you do need a vehicle for very frequent travels and use it regularly for family and kids- opting for your own transport might make more sense.

2. Walk if you need to get nearby than using your vehicle

Many of us get into the habits of riding our bikes or cars to nearby places just out of habit. Taking a walk is sometimes economical as well as adds to bit of exercise in your day.

We hope, if every one makes sense of this rule, the number of vehicles and the derived pollution reduces in India as well. It starts with me, it starts with you.

3. Maintain your vehicles

Regularly inspect and maintain your vehicles. This helps cut down on costs due to wear and tear. Instead of waiting for something to break down and incurring more unwanted costs, following a monthly schedule of maintenance will help save money.

4. Insure your vehicles

Do make sure to insure your vehicles. It is important to do so, to save on unforeseeable costs due to certain incidents. If you do not understand the basic concepts on insurance in India, we have put up a detailed guide here about vehicle insurance in India.

Tips for saving on lifestyle expenses

1. Buying gadgets and electronics: Upgrade only if it removes any inconvenience from your life.

Noticed the next iPhone ad ? Or the new Samsung galaxy? And now we want it. Many of us fall prey to needing the latest gadgets.

However, if you think over it- if the company had never released the new one or you had never seen the ad- you probably had the best device. You might not had the desire to upgrade.

Upgrade your devices, only if it removes any inconvenience from your lives. Don’t upgrade just because its being offered.

2. Invest in stock markets only if you know what you are getting into.

Many of us have lost money, by not knowing the investing game. Do take your time to learn the tools before you start investing.

Don’t jump into high risk investing if you don’t know what you are getting into.

There are various resources on the internet to learn about investments. Investopedia.com is where you can start with the basics.

3. Learn to cook

Do learn to cook to save on your food expenses. Cooking is an art and you never know if you would end up enjoying it.

Do make sure you eat a well balanced diet. Saving on costs by eating unbalanced diet is going to cost you on the long run.

Like my parents tell me, “What are you earning for ? You are earning, just so that you can makes the hospitals rich”. No offence to the doctors amongst us. However, not paying attention to your health is not cool really my friends. Taking care of your health is equally important as saving money. As the old saying goes- Health is wealth !

4. Avoid fast food

Even though fast food seems easy and cheap- avoid it whenever possible. Some fast food gets you addicted to it and that’s not something good, my friends. Saving money need not come at a cost of your health.

5. Bottle your own water.

Drinking enough water is healthy. Do carry your own water, if that helps you save cost. Invest in a good BPA free water bottle and carry it around with you.

6. Stick this message in your wallet

Print or write “Do I really need to purchase this ?” on a paper and stick or leave it along with your credit or debit card.

Every time you take the card or wallet out- you will be reminded of something and have a chance to reconsider your purchase before you swipe.

We have created some samples for you. Feel free to print them and keep it along with your credit cards.

Click here to download a free PDF version.

(Credit card size usually is around 85.60 × 53.98 mm (3.370 ×2.125 in)

7. Observe a no spend day

Mark a day on your calendar as a “No spend day”. If you can’t find one- remind yourselves of the day of the week you were born on. Let’s say it’s a Friday ? Every first Friday of the month shall be a no spend day ; )

Try to cook your own food, try not buying anything and no spending cash , no online shopping or swiping your card.

8. Pay credit card/ other bills on time – avoid fines

It’s is quite known to most of us that the interest rates on credit cards are quite high. So, one miss of payment – results in a large interest. So trying to pay your credit card bills on time should be one of the high priorities for us.

Also when you default on other bills, some organisations may levy a fine on the upcoming ones. It’s a good practice to automate other utilities bills and save on any fines.

9. For own good- quit smoking and alcohol

Smoking and excessive consumption of alcohol costs a lot on the long run. Not to say- what it does to your health with addictions.

Check how much can you save if you quit smoking by using our quit smoking savings calculator here.

How to start saving money when you are on tight budget

Saving money on a tight budget is challenging. Most of us loose hopes when it comes to these extreme points. But my dear friends, here’s a positive thing. Since you are already here, reading this article- you have got it started. As the old saying goes- “Where there is a will, there is a way ! “. Let’s find our ways with this attitude.

When you are on a tight budget and want to save money, you need to get your priorities right. This would come as something harsh, but begin with re analysing your needs and wants.

Needs are things you cannot live without. This basically means stuffs related to food, clothing and shelter. Most of us have gotten into the habit of defining wants as needs. The usual chatter in our heads is “But, I need it !” and we pin ourselves down to our wants.

Wants are stuff which may make your life easier, but you don’t really need it to survive. These are conveniences in your life.

Now that we have understood the basic categorisation, let us start assigning your day to day spendings. Once you have done that, re-visit each of them and find things that are wants and you can cut down on. You are not cutting them down for good. You can obviously have them, but only once you have met your goals of savings.

Once we have done that, let’s make sure we follow the budgeting methods discussed above and get started on our savings journey.

Along with the steps mentioned for getting started on saving in this article, we’ll also have to do the following steps as some extras. This is since we are on tight budget. Don’t worry- knowing what to do and when to do , wins us half of the battle. : ) We’ll get there.

1. Let’s begin with automating the savings plan.

When you are on tight budget, you are very prone to fall prey to excuses of not saving. We want to make sure, we don’t give ourselves this leak. Automate an amount you would be comfortable with. Have a look at second pointer below to decide the amount. But make sure you do automate this.

Save only what you comfortably can. Save a percentage than a fixed amount.

The recommended ideal amount of savings to build a buffer is about a quarter or half a year of your income. However, this may not be feasible for all of us , especially when we are on a tight budget.

Do check our 50/30/20 calculator and start saving a percentage. The ideal percentage is 20, but if you have variable income, a percentage than a fixed amount is better. If possible, we can also allocate the wants parts to our savings as well.

2. Save any unexpected income

When we say save a percentage, it also means saving anything more that’s possible. Sorry about this, but we are on a tight budget my friend. If you end up with any extra income, which you weren’t expecting- it would be good to save it. The goal is to get to our emergency savings buffer- as soon as possible.

3. Do expect and save for unforeseen expenses.

The worst thing that you might want to happen when on a tight budget is to loose all your savings in a go. If you have anticipated unforeseen expenses, you might have some buffer to play with. Even though you are on tight budget, saving a very small fraction towards such emergencies, will give you some breathing space and also keep you motivated on the savings plan.

Power of compounding- Save your money the best way

Now once you have learned all the tricks and tips to save money, parking the money in a proper instrument is also important. If you just leave your money , it may not may able to fight inflation. If your one rupee could buy you a pen today, not necessarily it can bring in the same tomorrow due to increased costs. Your money needs to grow along with the rising costs.

For beginners,

- Find banks in India, which gives you more interests.

- If you foresee not needing the money right away, it is a good idea to push that into cash or fixed deposits and earn higher income on it.

- Compound interest gives you income on your base amount as well as the extra interest you receive. Use the power of compounding and let your money grow.

Remember, money saving is not about cutting down- but being smart about it. It’s about being intelligent and optimising the flow. Make the right money moves my friends ! If you do like this article, please share this with someone who would benefit with these tips. Let’s work towards building a financially educated India! : )